The economic impact of climate change is rapidly emerging as one of the critical challenges of our time, reshaping how countries strategize for growth and sustainability. Recent studies indicate that the cost of climate change could result in extraordinary losses, with global GDP threatened by significant declines as temperatures rise. Projections reveal that even a modest increase of 1°C could lead to a staggering 12 percent decrease in economic output, an alarming figure that highlights the urgent need for effective decarbonization policy. As experts analyze economic forecasts, the stark reality becomes apparent: the financial repercussions of climate alterations could be six times larger than previously thought. Understanding the risk factors outlined in climate change studies is essential for securing economic resilience in the face of this overwhelming threat.

As we delve into the financial repercussions of global warming, the term ‘economic repercussions of climate change’ often comes to mind, encompassing various aspects including productivity losses and shifting investment patterns. This phenomenon entails not just a reassessment of traditional economic models but encourages a broader conversation about the sustainability of growth amid rising temperatures. Experts are increasingly focusing on how environmental shifts impact national wealth, and the associated costs of inaction could outweigh the benefits of proactive strategies aimed at sustainability. The role of policy-makers is pivotal in crafting regulations that address these pressing issues, ensuring that economic systems can adapt effectively to the challenges posed by a warming planet. Such strategic dialogue is essential for framing our future economic landscape in a way that prioritizes both growth and environmental health.

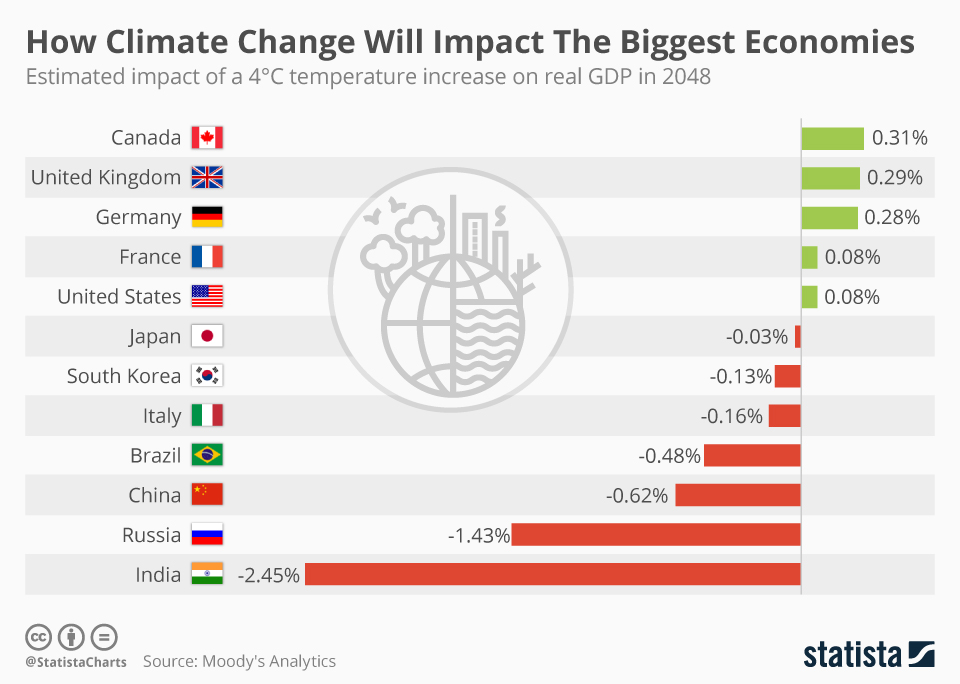

The Rising Economic Impact of Climate Change

The economic impact of climate change is becoming increasingly apparent as new studies emerge with alarming forecasts. Recent analyses indicate that the temperature rise by an additional 1°C could lead to a staggering 12 percent drop in global GDP. Such projections, significantly higher than earlier estimates, highlight the urgent need for reevaluation of the economic paradigms surrounding climate change. Adrien Bilal, a prominent macroeconomist, emphasizes that these findings should be a wake-up call for policymakers. As regions face more frequent and severe weather events, businesses may struggle to maintain productivity, thereby affecting national economic systems.

Moreover, the cascading effects of climate change could disrupt traditional economic forecasts, creating a ripple effect felt across various sectors. If global temperatures were to increase by 2°C, a 50 percent reduction in output and consumption could ensue, compared to historical precedents like the Great Depression. This level of economic impact suggests that failure to address climate change not only jeopardizes environmental stability but also threatens long-term economic growth. It is evident that timely interventions and decarbonization policies are essential to mitigate these dire economic outcomes.

Revisiting Economic Forecasts on Climate Change

The reconsideration of economic forecasts related to climate change introduces a more nuanced understanding of the potential risks involved. Traditionally, macroeconomists have underestimated the economic repercussions of rising global temperatures, predicting only minor reductions in productivity. However, recent studies are now showing that the cost of climate change could be six times larger than what was previously believed. This shift in perspective is crucial as it raises critical questions regarding the adequacy of current policy measures aimed at addressing climate-related challenges.

As Bilal and Känzig point out, the methodology employed to predict damages has evolved, taking into account a wider array of variables such as extreme weather patterns and their influence on economic performance. By analyzing data from 173 countries over a 120-year span, they highlight the complexity of accurately forecasting economic impacts. Incorporating these new findings into future economic models will not only improve the accuracy of climate change studies but will also better inform policymakers on the potential need for more aggressive climate action.

Frequently Asked Questions

What is the economic impact of climate change on GDP according to recent studies?

Recent studies indicate that the economic impact of climate change on global GDP is significant. Each additional 1°C rise in temperature could lead to a 12% decline in global GDP, which is six times larger than previous estimates. This suggests that climate change poses a serious threat to economic productivity and growth.

How are climate change economic forecasts created?

Climate change economic forecasts are developed using models that analyze historical weather data and economic performance. Recent methodologies consider global temperature changes and their correlation with extreme weather events to produce more accurate predictions of economic fallout, offering a clearer picture of the cost of climate change.

What are the costs associated with climate change and decarbonization policies?

The costs associated with climate change have been assessed in various studies, with the global social cost of carbon estimated at approximately $1,056 per ton. In contrast, federal decarbonization measures, such as those outlined in the Inflation Reduction Act, are estimated at $95 per ton, indicating that effective decarbonization policies can provide economic benefits.

Why is understanding the economic impact of climate change important for policy-making?

Understanding the economic impact of climate change is crucial for effective policy-making because it provides insights into the long-term costs of inaction. Better economic forecasts related to climate change allow policymakers to evaluate the cost-effectiveness of decarbonization policies, ultimately driving sustainable economic growth.

What is the projected economic toll from an additional 2°C rise in global temperature?

If global temperatures rise by an additional 2°C, projections suggest a 50% reduction in output and consumption, which would be more severe than the Great Depression. This highlights the urgent need for climate action to mitigate such drastic economic impacts.

| Key Point | Details |

|---|---|

| Economic Toll of Climate Change | Recent studies show that projections of economic impact from climate change are six times larger than previous estimates. |

| GDP Impact of Temperature Increase | Each additional 1°C increase in global temperature could lead to a 12% decrease in global GDP, peaking six years after the temperature rise. |

| Comparison to Previous Studies | The recent estimates by Bilal and Känzig argue that the economic consequences of climate change were previously underestimated by macroeconomists. |

| Economic Growth vs. Climate Change | While economic growth is expected to continue, climate change could reduce potential wealth significantly by 2100. |

| Social Cost of Carbon | The study estimates the social cost of carbon at $1,056 per ton, contrasting sharply with previous estimates of $185 per ton. |

| Decarbonization Relevance | Findings suggest that decarbonization policies would be beneficial economically, especially in larger economies. |

Summary

The economic impact of climate change is profound and alarming, as recent studies have revealed. New projections indicate that the economic costs associated with climate change could be six times greater than earlier estimates, highlighting an urgent need for action. The continuing rise in global temperatures is linked to significant GDP losses, with a potential 12% decline for each additional degree Celsius. Furthermore, the social cost of carbon has been reassessed, indicating that carbon emissions have a much higher economic penalty than previously believed. It’s clear that without decarbonization efforts, the economic future may be severely compromised, with an emphasis on sustainability becoming not just beneficial but essential for long-term economic wellbeing.